Stock market volatility can be unnerving. No investor, whether they’re new to investing or have been making deposits for years, likes to see the value of their portfolio go down—even if it’s just temporary. When the market takes a turn, some people will inevitably sell investments in an attempt to minimize their losses, while others will stop making new deposits to their investment accounts. Unfortunately, both are mistakes that can cost you in the long run. Instead, you should do nothing. Don’t make any changes to your strategy: just keep investing on a regular schedule even when the market is down. Why? History shows that markets have behaved predictably in the long run, and investors who stay the course are likely to come out ahead.

We know this can be tough to do, and we want to help. So in this post, we’ll provide some historical perspective on past market downturns so you can feel more confident that you’re doing the right thing for your portfolio, even when markets are turbulent.

Market declines are very common

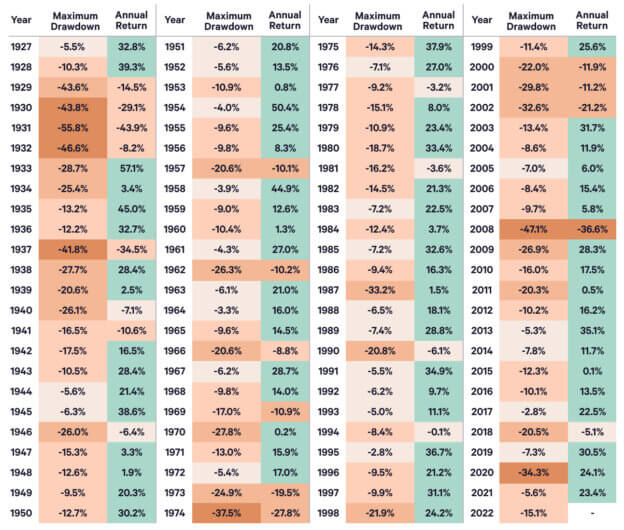

Market declines can rattle investors, but it’s important to keep in mind that they’re very common. The chart below shows the maximum drawdown (this is the largest loss experienced over a certain time period, expressed as a percentage) of the US stock market every year since 1927 as well as the market’s total return that year. As you can see, large drawdowns (or declines from a recent peak) are extremely common. And you might be surprised to learn that even years with large declines can still yield impressive positive returns for investors at the end of the year.

Source: Kenneth R. French Data Library

For example, let’s take a closer look at 2020 when US stocks entered a bear market. The market had a maximum drawdown of 34.3% that year, which is large even by historical standards. But investors who stuck it out all year were rewarded with a total return of 24.1% by the time the year was over. Of course, in order to get that return, an investor needed to stay in the market and avoid missing the recovery. The lesson here is clear: history shows that if you stayed invested when the market was volatile, you likely came out ahead.

Historically, the market has gone up in the long run

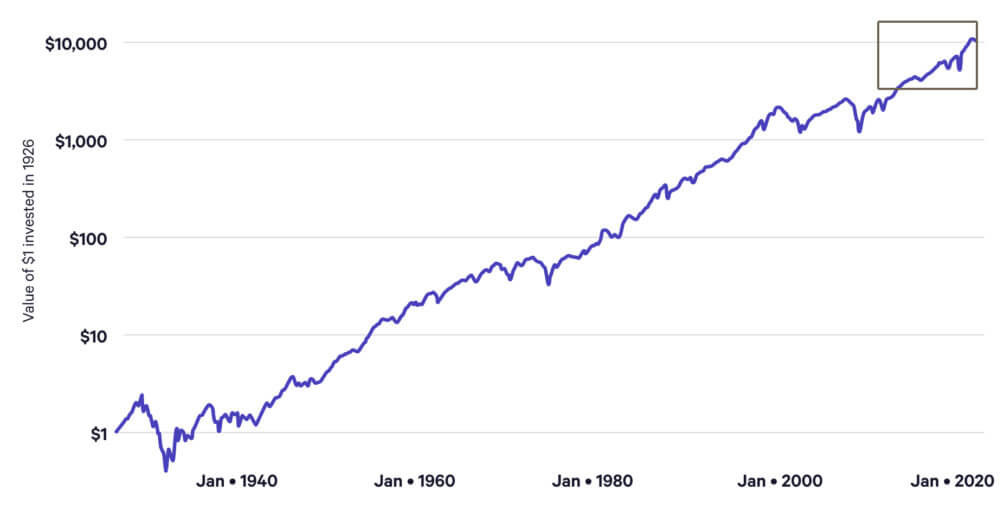

Temporary declines like those in the table above can certainly be nerve-wracking, but if you have a long investing time horizon, they’re just blips on the radar. You can see this clearly if you zoom out and look at the behavior of the US stock market since before the Great Depression: the overall trend is up and to the right.

To help you visualize this, we put together a chart showing the value of a dollar invested in 1926. The point isn’t that you should have invested a dollar nearly 100 years ago, although that would have yielded impressive returns—it’s that the US stock market has behaved unpredictably in the short term but fairly predictably in the long run. (Note that the scale of the y-axis is logarithmic, not linear, enabling you to see fluctuations more clearly. The box in the top right corner highlights the last 10 years.)

Value of $1 invested in the US stock market 1926-2022

Source: Kenneth R. French Data Library

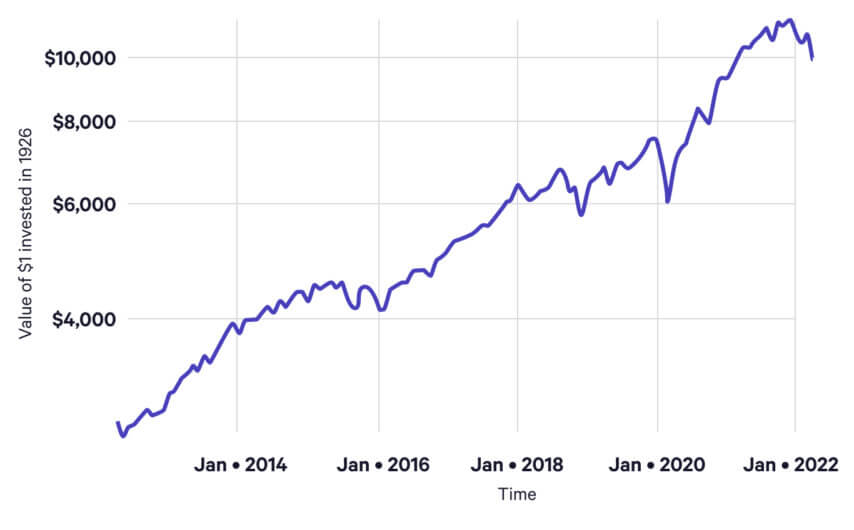

Of course, the last few years have been extraordinary in some ways because of the COVID-19 pandemic. However, those events still haven’t altered the overall trajectory of the market. Below, we’ve zoomed in on the section of the chart covering the last 10 years. As you can see, the overall trend of the broad US stock market is still very clear: it goes up. History has shown that even in the case of a bear market (a decline of 20% or more from a recent high), the market tends to recover much faster than you might think.

Value of $1 invested in the S&P 500 in 1926, 2012-2022

Source: Kenneth R. French Data Library

The bottom line

We encourage you to see short-term stock market declines as an opportunity: if you keep putting money in the market, you effectively get to buy investments while they’re “on sale.” Plus, you can lower the taxes you’ll pay with tax-loss harvesting. Wealthfront offers automated Tax-Loss Harvesting to our clients at no additional cost, which in 2021, generated tax savings worth between 4 and 9 times our advisory fee. That’s like getting an extra 1.8% on top of your returns.

Periods of volatility are a good reminder of the importance of diversification—or buying a wide range of investments instead of focusing on a single company, sector, or geography. Diversification can increase your risk-adjusted returns and, to some extent, insulate you from losses. When you feel insulated from losses, it’s easier to stay invested, which is key to investing success.

You might hear people talking about “buying the dip” or waiting until the market bottoms out to begin investing again. This sounds good in theory, but it rarely works out in practice. That’s because in the moment, it’s virtually impossible to tell whether the market has hit bottom or will continue to fall. There’s also the opportunity cost of sitting on uninvested cash waiting for the bottom. Unfortunately, academic research has consistently shown that timing the market doesn’t work—even most professional investors can’t consistently get it right. That’s why we think it’s wise to stick to your investing plan regardless of what the market is doing.

We hope the information in this post helps you feel more confident about staying the course with your investments. We know it’s tough, but you’ll be glad you did.